Unveiling the Power of Microcaptive Insurance

Welcome to an exploration of the power and potential behind microcaptive insurance. In today’s ever-evolving business landscape, companies are constantly seeking innovative ways to manage risk and optimize financial strategies. Enter microcaptive insurance, a unique and increasingly popular solution that has caught the attention of businesses both large and small. Captive insurance, as a concept, has been around for quite some time, but microcaptives in particular have gained momentum due to the unique benefits they offer. In this article, we will delve into the intricacies of microcaptives, shedding light on their purpose, advantages, and the important details surrounding IRS 831(b) tax code. So, let’s embark on this journey and uncover the potential that lies within the world of microcaptive insurance.

Understanding Microcaptive Insurance

Microcaptive insurance, also known as captive insurance under IRS Section 831(b) tax code, is a type of self-insurance strategy that has gained popularity among small to medium-sized businesses in recent years. This unique form of insurance allows these businesses to form their own insurance company, or "captive," to provide coverage for their specific risks.

By leveraging the benefits of captive insurance, businesses can gain greater control over their insurance costs and tailor coverage to their specific needs. Unlike traditional insurance, microcaptive insurance is not available to the general public and is exclusively designed for the participating businesses.

One of the key advantages of microcaptive insurance lies in its tax benefits. Under IRS Section 831(b) tax code, microcaptive insurance companies can elect to be taxed only on their investment income, rather than their total premium income. This can result in significant tax savings for businesses, allowing them to channel funds towards their core operations or further investment opportunities.

In addition to tax advantages, microcaptive insurance offers businesses greater flexibility in managing risks. By establishing their own captive insurance company, businesses can customize coverage, set underwriting guidelines, and even participate in policy decision-making. This level of control facilitates a more strategic approach to risk management and ensures that coverage is tailored to the unique needs of the business.

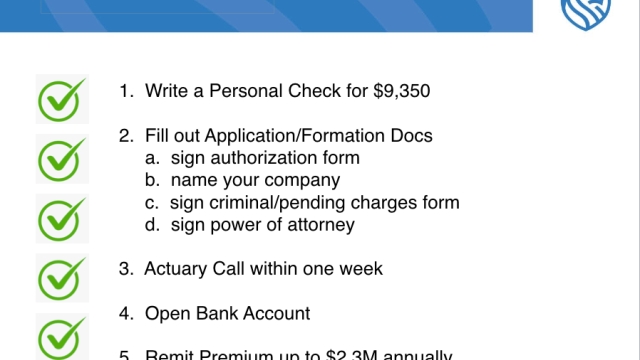

As more businesses recognize the potential benefits of microcaptive insurance, it is essential to have a clear understanding of the intricacies involved. The subsequent sections of this article will delve deeper into the process of setting up a microcaptive, the regulatory framework encompassing it, and the key considerations for businesses contemplating this insurance strategy.

Benefits of 831(b) Captive Insurance

Microcaptive insurance, also known as 831(b) captive insurance, offers several compelling benefits for businesses. This section will delve into three key advantages that make this insurance option a powerful tool for risk management.

Enhanced Risk Management: One of the primary benefits of 831(b) captive insurance is its ability to provide tailored risk management solutions. By establishing a microcaptive, businesses gain greater control over their insurance coverage. Unlike traditional insurance, microcaptive insurance allows companies to customize their policies according to their specific risks and needs. This personalized approach ensures that businesses are adequately protected while reducing coverage gaps that may arise from standard insurance policies. With the freedom to design bespoke insurance solutions, companies can manage risks more effectively and mitigate potential losses.

Read MoreTax Benefits: Another major advantage of 831(b) captive insurance is the potential for significant tax savings. Under the IRS 831(b) tax code, microcaptive insurance companies can qualify for special tax treatment. Premiums paid to the captive insurer are tax-deductible for the parent company, thereby reducing the overall tax burden. Additionally, microcaptive insurance allows businesses to accumulate reserves that are tax-exempt up to a certain threshold. Through these tax advantages, companies can optimize their financial strategies, enhance cash flow, and allocate funds towards further growth and development.

Asset Protection: Microcaptive insurance provides an effective means for safeguarding a business’s assets. By establishing their own captive insurance company, businesses can protect their assets from various risks, such as litigation, catastrophic events, or unexpected losses. With proper risk assessment and coverage, companies can shield their wealth and ensure continuity in times of adversity. This asset protection aspect of microcaptive insurance enhances the overall financial security and resilience of businesses.

In summary, 831(b) captive insurance offers a range of benefits, including enhanced risk management, substantial tax advantages, and asset protection. By leveraging microcaptive insurance, businesses can optimize their insurance coverage, reduce tax liabilities, and protect their assets effectively. Understanding and harnessing the potential of microcaptive insurance can empower companies to navigate risks with confidence and achieve long-term financial stability.

Navigating the IRS 831(b) Tax Code

In order to understand the workings of a microcaptive insurance company, it is essential to navigate the IRS 831(b) tax code. This tax code specifically addresses the unique taxation rules applicable to small insurance companies known as captives. Understanding the nuances of this code is crucial for individuals and businesses looking to leverage the benefits of a microcaptive.

Under the IRS 831(b) tax code, a qualifying captive insurance company can elect to have its underwriting income taxed at a lower rate. This tax advantage is one of the main reasons why captives, especially microcaptives, have gained popularity in recent years. By electing to be taxed under section 831(b), these small insurance companies can potentially enjoy significant tax benefits.

However, it is important to note that the IRS has implemented certain restrictions and requirements for qualifying as a microcaptive under section 831(b). These requirements include meeting specific premium thresholds, limiting the types of risks a captive can insure, and ensuring adequate risk distribution among policyholders. Navigating these regulations is crucial to maintain compliance with the IRS and fully utilize the benefits offered by the tax code.

As with any taxation matter, it is highly recommended to seek the expertise of a qualified tax professional to ensure proper compliance with the IRS 831(b) tax code. They can assist in structuring a microcaptive insurance company in a way that maximizes tax advantages while also ensuring adherence to all legal and regulatory requirements surrounding captives. By navigating the intricacies of this tax code, individuals and businesses can unlock the potential power of microcaptive insurance and the advantages it offers.